Jenni: Welcome to Modern Family Finance Podcast, where we talk about all things, money, career, and life. I'm Jenny, your host and founder of Modern Family Finance, a fee only financial planning firm in the San Francisco Bay area, with the mission of providing tech smart financial advice for modern families.

Delivered like a trusted friend. So I am really excited about today's guest, Katie Burke, because she is someone whose work touches so many of the big life transitions our clients navigate. And she's also been someone who has been a part of our San Francisco community. So Katie and my wife Lisa, actually sang together in the Glide Memorial Church Gospel Choir in the Tenderloin for many, many years.

When she's not doing that professionally. Katie is a San Francisco based family law attorney and the founder of Bir Law. She brings over two decades of experience helping individuals and families through everything from divorce and custody to pre-marital and post-marital agreements with the background in psychology and a deep understanding of dynamics within relationships, she approaches these conversations with clarity, compassion, and a very modern sensibility.

Which, you know, we love around here. So Katie, I am excited to have you here today.

Katie: I am excited too. Thank you for having me here.

Jenni: Cool. Well, I know you have a background in psychology. I would love to hear your journey of how you got into this work.

Katie: Yes, so I got a earned a BA in psychology and then a Master's degree in counseling psychology. I was always gonna be a psychologist. And halfway through my master's program, I was a huge ally McBeal fan during that time and really, really interested in, started getting more interested in law and decided rather than.

Sit with people and work through their problems, you know, face to face. I'd rather just do something with the problems and take it and run with it. So that's how I ended up going to law school and and that's ultimately how I ended up in Family Law

Jenni: Awesome. Great. And where are you based out of?

Katie: San Francisco.

Jenni: Francisco. Okay, great. Okay, so I want to focus our conversation about premarital, and I guess we can call it postmarital agreements too, if you already are married. And because I personally believe that this is a really important topic that kind of has a bad wrap.

And when couples hear the term premarital agreement, they often pictures like. Bazillionaires in a bad romcom. So can you start by just grounding us what these type of agreements are actually meant to do.

Katie: Yes. So they're meant to protect what each person brought into the marriage, if that's what they wanna do, which is commonly what they wanna do. Also what they might inherit, what they might have come in during the marriage that they're already anticipating. It's really, it can be a tool for what they're looking to protect individually.

Also to equalize and stabilize things. Some people come to me and they're looking to be generous. But also be generous in a smart way. So if there's a really pronounced imbalance between the two parties and the couple sometimes the one who is the higher earner and or higher asset holder. Doesn't wanna have that kind of imbalance dynamic.

They wanna balance it out. So they wanna try to figure out what's the most fair way to really set the other person up to not feel like they're at a total disadvantage during the marriage, but also if there's a separation and divorce. And then also it's a way to have a clear understanding of what each person expects.

So in my premarital agreements and postmarital agreements, I often will put in provisions that are not gonna be enforceable if they separate, because at that point they've already separated, but they're provisions that are marital provisions. Just so they've talked about it, thought about it. Put it down in writing, and again, nobody's gonna enforce those ones, but it's just a way to get them thinking about it.

So for all those reasons, protecting oneself, being generous to the other, and setting forth expectations.

Jenni: Awesome. Well, when you, when people come in or when you talk to people about these type of agreements, what are some of the biggest misconceptions you hear?

Katie: One of them is a really big one is people will say, oh, we don't really have a lot, so this will be really simple. You know, people are always cost conscious no matter what they have. And also just want things to be simple. And the misconception there is that regardless of how little or how much someone has, they're going to get the same density of.

Content in their agreement. So mine tend to be 30 pages single spaced, and you're gonna get that if you don't own anything to your name or if you, you know, own a multi-billion dollar corporation, you're gonna have basically the same. Not, basically, you're gonna have the same level of detail about every single thing that could possibly happen for a couple of reasons.

One of which is you don't know what the future holds. So when you're drafting a premarital or postmarital agreement, you're drafting categorically. You're not only drafting for what already is you're drafting, so that. Hopefully you don't have to amend it. It's not like an estate plan where you get a new asset or a new liability and you need to amend it with a pre or postmarital agreement.

If you've drafted it correctly, you don't really have to amend it for that reason. There can be other reasons you'd need to amend it, but so one reason is, you know, you're, you're doing things categorically. Regardless of the simplicity or complexity of the assets or income. And so that's one misconception.

And then the other one is just the, this I hear less and less, but kind of people have said before, you know, oh, don't you just pull, you know, something out of a form book and. No, definitely not. I have my own templates, but they're mine and I've created them and I'm constantly, constantly changing them and there's a lot of customization that goes into them.

So those would be the biggest misconceptions is that there's some way that they would be simple and that of course they would be simple. 'cause this just comes out of a form book.

Jenni: Got it. Well, you know, is there, can you maybe describe some of the common types of couples in, you know, in general forms? Like what, what kind of people do you end up working with for Prema when it comes to premarital agreements specifically?

Katie: There are a lot of people whose parents want them to get one, so they don't necessarily feel strongly one way or the other, but their parents have said, I want you to get one because you're gonna inherit money. That's a big one. And I'd never worked directly with the parents. I don't communicate with the parents at all.

But, but I know that that's why they're, they're doing it. Another type of client is somebody who. Has amassed a lot of wealth before marrying, maybe they were married before, or they just are marrying older, or they just have a lot of wealth. So they're looking to protect that wealth and or as I said earlier, they might be wanting to distribute that wealth even during the marriage and, you know, and, and be generous.

And then there are a lot of people who are similarly situated to each other, but they just. Understand that this is a good idea and they wanna do it. And so they're just very proactive people. So there's not, I don't really have a typical client because there are so many different reasons people would do this.

Jenni: Yeah, that makes sense. What would you say if, you know, you're talking to one person and the couple who wants a par premarital agreement, but they're afraid to be for, for maybe any of the three reasons that you mentioned. Right. But they are afraid. They don't know how to bring this up to their partner.

They don't wanna kill the romance. How would you suggest they bring this up?

Katie: , Here's how I'll say it. Someone said this to me.

Once everybody has a premarital agreement, if they're getting married. It's just, do you want the state's premarital agreement or do you want your own? So if somebody is worried that it's gonna seem like they're protecting themselves in case of divorce, there are codes and statutes and cases already in place to address that eventuality if it happens.

So that's one thing I would say. And then the other thing is that they can say to their partner, I just wanna have something that's really clear so that we can move forward and just be. Happy, you know, we don't have to worry about it. So it's a delicate situation. A lot of times it depends on why they're doing it.

Of course, it's much easier if they say, my parents want me to do it, because that's, that's the reason. So there would be all kinds of different reasons and it's. I, I don't think I've ever had anybody who was actually thinking they were gonna get divorced, so it's, I think it's a pretty easy conversation to have when people are in love and they trust each other, that that's not what they're thinking is gonna happen.

There's some other reason they're doing it.

Jenni: Yeah. Yeah, that makes sense. And if a couple is thinking about getting married or, you know, they're thinking about the premarital agreement process, what is the ideal timeline that they should start doing this? Is there

Katie: I think that whenever, you know, as soon as they get engaged, I think is a good idea because then they know what the date is. You know, I've had people come to me and say. Oh, the other person hasn't proposed yet, and that's too soon because you don't know. You know how long this is gonna be. And I mean, very, very often people hire me and we're talking premarital agreements now, but very often people hire me and they don't know when the wedding date is.

So there's still that kind of long tail potentially, but at least there's an engagement. They're in forward motion, and it can sometimes be too soon because. Part of doing premarital agreements and postmarital agreements is financial disclosures and those can get stale. So that's why I say if somebody, there hasn't even been a proposal yet.

They're not engaged yet. I say, come back when you're engaged. But other than that, I mean, even a year in advance is okay and there may be some updating of the financial disclosures, but I'm a big fan of getting things done early six months I think is really ideal. Most people wait until three months or less.

Even, even with really complex assets and income, you know, 'cause it's really, the reasons for waiting or getting ahead of it are really psychological, I think a lot of the time and. I used to say I wouldn't work on one if they, if the wedding was three months or less away. And then I realized that's actually most people.

So that's when I started really templatizing and systematizing the process so that I could work really quickly once they come to me. But, but six months I think is really ideal. But as I said, if they're engaged, even a year is good. But if, if it's like a three year engagement or something, they know that it's gonna be way off.

That will be too soon.

Jenni: Got it. Okay. All right. Well, I mean, kind of now thinking about you know, we work with, with households of all different shapes and sizes, and so there's, you know, we work with a lot of L-G-B-T-Q couples. We also work with couples who are together, but not necessarily married or even intending to be married.

So when we think about kind of these non-traditional households, how does a premarital agreement fit in, if at all? I guess when it comes to the, yeah.

Katie: Right. So another type of agreement I do is called a cohabitation agreement, or sometimes I don't even call it that because sometimes people don't even live together, but they're intimate partners. But if they. Don't plan to get married or the wedding that they're planning or the, or they think they will get married, but it'll be so far off in the future.

But right now they wanna get real estate together or something like that. Then I do either, I call it a cohabitation agreement, or sometimes I call it an intimate partner agreement. Doesn't really matter what the title is, but the idea is these are people who either will never get married or are not getting married anytime soon, but have wanna put these protections in place.

So that's one thing to think about. I used to do, you know, many, many years ago before, what was AB 2 0 5 was the year 2005. I would do many, many, many more cohabitation agreements and now there're fewer because people can get married. But they do come up a lot. And it can be same sex couple different sex couple, I mean, lots of reasons people wouldn't get married.

But with the cohabitation agreement, I'm doing the exact same thing I am making sure that. Whatever protections they want in place are there, and whatever protections they don't want each other to accrue are also written out and very explicit. And then you know, another thing to think about is with LGBTQI Plus in general, is that now more than ever, the laws we thought were foundational are subject to change.

You know, we know that now more than ever, so or even being completely demolished. So a lot of times. When people come to me for a premarital agreement or postmarital agreement, they're really asking for things that the law protects anyway. But even many, many years ago, I was a big fan of the agreements and I just thought, you just don't know how something will change.

And it's really, really good to have your intentions written down and written down very clearly. So you know, that's another thing I I like for people to think about is just codify whatever it is you're looking to protect into your premarital agreement.

Jenni: Yeah, well, I mean, you bring up a really, like we key point here, which is that we don't know what's, you know, the L-G-B-T-Q-I things that we thought were kind of firmly in place, feel less firm now. So specifically for couples for L-G-B-T-Q-I couples, even if they are married, is there anything in particular kind of specifically that you would suggest that they do?

Katie: I mean, I just think having an agreement is really important. Often estate planning is really important too. I don't do estate planning, but I give referrals. To estate planners. And I think, you know, I mean, I think so far marriage is still legal among, you know, any same sex couples, so there isn't really anything special now, and there hasn't been since 2005, which is when AB 2 0 5 took effect.

And and if any of the listeners don't know what AB 2 0 5 is, it was the law that starting January one 20, did I say 2025, 2005? That starting January one of that year, 2005, any registered domestic partners were automatically opted into to basically the, the privileges and responsibilities of marriage in California, but not federally recognized.

So I, I give that marker because that is still. When there was a real change between what was before and what is now, and at least as of now, all the protections for same-sex couples are still in place. So there isn't really anything specific other than just, it's just a good idea to have these, these items written down.

Jenni: Okay. Got it. So like what you're kind of, just to summarize, I think even if you're a married queer couple right now, they're, you're still fine, I guess, according to law, right? But you're kind of saying, look, given that there is some shakiness here would be still good idea to have some of these agreements.

And I guess in this sense it would be like a post post-marital agreement, right? Where a lot of

Katie: Depending, yeah. Where they are in their marriage trajectory and, and the other, you know, way closer to 2005, but after 2005, one of the biggest considerations in any of these agreements would be how much. Investment financially, the two would ha would've had in each other for so long before they were allowed to get married.

And actually they, it wasn't 2005 when they were allowed to get married, but anyway, long ago. That was a but much bigger consideration than it is now. Now that marriage has been around so long. Whether a same sex couple has gotten married or not, it's just different than it was back then. And, and because there was so much that was legally unprotected, but it could have been decades when they were together and amassed property.

So there would be much stronger considerations to think about back then. But now it, it's, it's not as much an issue. You.

Jenni: Okay. Got it. Okay, so kind of talking about kind of in the same vein, let's talk about California's community property loss, like what you said earlier, which is like, if you don't have a plan, if you don't have an agreement, there is a default agreement in place. Okay. So if you had no agreement, premarital or postmarital, what does California say is going to happen in the event of a separation?

Katie: Well, it, it sort of depends issue by issue. But the law generally aims at a 50 50 division of marital assets and debts. And there are nuances to that, whether we're talking about retirement accounts, whether we're talking about income, which is neither an asset nor a debt legally. But you know, whatever real property, whatever we're talking about, there are some nuances.

But in general. The law in California aims at a 50 50 division of assets and debts from marriage and income being community income as well. 50 50. And one of the things I, you know, would want people to think about with that is something that comes up sometimes is that if a marriage has been strained for a while and one party is really carrying the other financially, sometimes if they come to me for a divorce.

They're like, I can't wait to stop supporting this person. And I'm kinda like, uhoh, how long have you been supporting them? Because the longer they've been, longer that other, that other person has been relying on, let's say my client, is the person relied upon. The longer potentially the tail of spousal support might be because the law is trying to protect if, if someone relied on the marriage heavily financially.

California isn't gonna just kick them to the curb with no money. So a lot of times someone will come to me and they're just done. And it's like, well, you're not done, you know? And then they said, well, then I should have left them years ago. And it's like, well, too late now. Their argument will be, I shouldn't have to support them.

I supported them all these years. But actually, I always say, you're making their argument. You know, if you supported 'em, that's what they relied on. So I think it's important for people to think about that because. If they, there is a lot of resentment for people sometimes if that's the reason they come to me and they kind of stuck it out for a long time and they wanna be done and, and it's not gonna happen that way.

Jenni: Yeah. Interesting. Are there any other kind of parts of California's community property laws that catch people by surprise that you wish people understood before? Either they got married or otherwise.

Katie: I don't think so. People seem pretty like they seem to really understand the laws now. I think people just have a general lay sense that, you know, everything gets divided by half, you know, in half. So, yeah, there aren't a lot of real surprises. I mean, there are things that are really black and white and simple that you might not think would be like retirement accounts.

The law is very, very black and white there, so unless the parties agree to deviate, it's going to be a half and half. You know, what accrues during the marriage, regardless of who the employee or self-employed person is. And to some degree that's also true about restricted stock units and similar assets that there's kind of a formula.

So it makes it simple in the sense that there isn't a lot to argue about because the law is really clear. Places where the law is very gray, permanent spousal support is one of those, and it's called permanent, but it really just means post-judgment. You know how much support someone's gonna get and for how long.

After the judgment is entered that is a place where there's a lot of figuring out to do because there isn't a numerical formula. There are subjective factors to look at. There's a statute that covers that family code section 43 20, but it gives you nothing in the way of a formula like there is for temporary spousal support and for child support.

So I think that's surprising for people that they can't just know. You know, in my first consultation with people, I can't tell them what permanent support is gonna look like. I can give them ideas, but duration gets kind of murky and the amount gets kind of murky because they're just harder to figure out than something clear cut where the law is easy.

Jenni: Got it. Speaking of like, you're kind of saying it's all 50 50, the stuff that is generated in marriage, but can you help can you kind of explain a little bit? More about like the separation. If the, if, if someone is coming into the marriage with a lot of assets and then during the marriage, there's also gonna be more assets.

Like what about the stuff before the marriage? Is that kind of safe? Even if you don't have a premarital argument? Sorry. Argument, agreement.

Katie: It, it is usually safe. There's something called transmutation, which family code section 8 52 governs that and people can transmute an asset from separate to community or community to separate or from one party, separate to the other party separate by a writing signed by the party adversely affected.

So. If you haven't transmuted an asset in that way that you brought into the marriage, generally speaking, those assets are safe. One of the reasons people like to have a premarital agreement is just to not even have that door opened, you know? So a lot of times that's what's happening in an agreement, but generally speaking, those things are safe.

Inheritance to one person, even during the marriage is separate property. And again, tends to be safe as long as it isn't transmuted. I have, in some of my premarital agreements, I draft a provision that says if somebody moves their own separate funds into a joint account, a community account and keeps them in there for 45 days, that transmutes it without assigning.

That's not the law, but that's just something some people like to do. If they say, I just wanna be able to share money and not. Have everything have to be a signed document, you know, so that's a way to make sure if you make a transfer accidentally, you haven't just turned some huge sum of money into community property that you didn't mean to.

But short of those things, you know, you, you can't sort of just accidentally change something that you brought into the marriage, into community. But, but when divorce happens, there can be a lot of arguments about. Either the assets themselves or if they're income producing assets, the income from those assets.

Jenni: Can you give us some kind of specific examples where it's like, because they did not have a primarily agreement, these were some areas that got fought about in the divorce that were harder to defend?

Katie: This is one, this is one's a little bit random, but it's one that comes up all the time, which is gifts from parents. Because when people are married, everybody's considering it a gift to the couple because there's no reason to not think that. And then in a divorce there can be a lot of dispute and those gifts can be really substantial.

And it can mean hundreds of thousands of dollars in some cases maybe even more. And so that's something that's just. Something I have people consider for any premarital or postmarital agreement. How are we going to prove what that is on separation, divorce? How are we gonna categorize it? Let's just do it now.

So my horror stories come from handling divorces, and that's how I figure out, you know, what I wanna put in my premarital agreements. So the parent gift is a big one for that. And another one, another one. I mean it's really sort of the bigger the asset or sometimes someone will come to me and it doesn't even necessarily have to b be a big one, but they'll come to me and say, what I really wanna make sure if we ever got divorced I have is this, you know, a retirement account I brought in or something.

And, even if the law might protect it, it can be depending on the dynamics with the couple when they divorce, somebody can really threaten to go after it. If there's not good evidence, if they were married for a really long time, records disappear and banks sometimes don't have records. If you go far enough back, it can be really hard to get bank records.

So, anything, even if it seems really clear in the law, could be problematic if you have to do a really involved tracing to prove what you already know is true or if the records could be gone because so much time has passed.

Jenni: Got it. Yeah, so it's, yes. So I'm kind, I am asking the question of like the horror stories. If you don't do a premarital agreement, these are the things that might get you later. Right. And you mentioned this whole individual account to joint account question. You know, it, let's assume the couple does not actually have agreement.

They're married and the. One person has assets from prior marriage and then they retitle into joint and they don't, they're not really thinking about this. They're just thinking mutually, we need to use this to buy the house or whatever. Have they basically transmuted this?

Katie: Retitle what to joint

Jenni: The money Let, yeah. Let's say they came, they came into the marriage of the million dollars from before the marriage.

Right? It was in their own account. Now they, now it's moved into a joint bank account because they were gonna buy a house together, let's say,

Katie: Bank accounts don't, bank accounts are not really. Joint or separate in that way, people think sometimes whoever's name it's in, which has nothing to do with it. It's really the funds themselves. So the funds are what you're tracing to figure out. And, and again, family code section 8 52 governs transmutation.

So you couldn't transmit mute just by putting funds into an account. So that's why I was saying sometimes I have a provision in my premarital agreement that allows you to transmute by just moving it into an account,

Jenni: So.

Katie: and keeping it

Jenni: Got it. So if they, in this example, if they moved a million dollars from an individual account into a joint account, you could still trace it back and say, look, this was money I had before, therefore it was not.

Katie: It's the money you're following, not the account, and definitely not whose name the account's in that has, and, and that's a common misconception. People think it matters whose name it's in. It doesn't.

Jenni: Gotcha. Okay. So

Katie: But that's, you know, that's another horror story that reminded me because people get really hung up on whose name the credit card was in, or even who used it doesn't even really matter who used it.

You know, if it was for regular, everyday, you know, even if it was that person's gym and they're the only one who used the gym, that's still considered marital use. So things like that surprise people that, you know, your everyday comings and goings, even if it had nothing to do with the other person are still marital and community.

Jenni: Yeah. Got it. Okay. Okay, shifting, shifting gears a little bit. So when you see a couple, and there is kind of in one of your examples, like if a couple comes in, one person has a big discrepancy in income or assets, what are some, you know, what are some of the solutions or ways in which you have helped them kind of address this that they don't, like you said earlier, there might be a couple that comes and says like, I actually want this to feel more fair or.

I guess that's one example. Another example might be, I want to go into this without worrying that I might lose my assets in. In either case, how do you help the couple address this friction point so they feel like it's fair if there's a big discrepancy.

Katie: Yeah. I, you know, some ways it's happened is I had a client who. Wanted to buy. He had many, many parcels of real estate and he wanted to buy a parcel of real estate for his fiance so that that could be completely hers. And then we put in the premarital agreement that that was a hundred percent her separate property asset and any rental income that came from that asset would be her own.

And that's an example of somebody who wanted her to feel like she had her own security in the marriage. And it wasn't just. You know, she had whatever little money she had and she was depending on him. I've had people add someone to title. You know, with very strong warnings that it's, you know, I mean, I always like to warn my clients that it's like, you can choose to be as generous as you want in a divorce.

No one's going to stop you from being generous if you want to, but if you put these things in the premarital agreement or you add someone to title, you have now made that the law. But sometimes, I mean, people are coming from that place where they say, that's what I want. I don't want somebody. To feel unwelcome, you know, into this life that I've created.

Another one is I had somebody, and this, this could feel weird for some people, but it didn't feel weird for this couple. He was giving her an allowance every month. And that was also so that she would have her own money, and we wrote it as her money. So it's, there's no going back on that. So during the marriage, that was her money.

And in the event of divorce, that would just have been her money gone or still there. And so those are some ways, and it's really anything anyone can think of because the only way a judge is going to interfere with any ideas like this are, what they're looking for is unconscionability. And that's the legal term, but it also is what the lay term means.

You know, if they look at something and they say. This is just nobody would've, this offends my conscience whether you were okay with it or not. So no judge is going to be offended by, you know, someone being Yeah. Unless the generosity swings so much the other way that you know, that that person's poor.

But but yeah, so, you know, something like that, or, I mean, another way a judge would set something aside is if it's not validly. Drafted and signed and notarized and all that. But apart from that, if it just seems unconscionable other than that, I mean, so those are some ideas, but people can really think of anything they wanna think of.

Jenni: Yeah. Yeah. Okay. So yes, that, that's helpful. And those are great ways. I mean, yeah, it might not make sense for everybody, but I could see how it can make sense so that you're, you feel like you're entering a partnership with fairness and that the other person feels fully secure, right. Okay. So another topic.

Let's talk about kind of stock. We talked a little about like stock options and RSUs. Many of our clients kind of have those and founder shares. Some of them might have been earned before marriage. Some of 'em might earned after marriage. Maybe it was valued very little before marriage and then appreciated after marriage.

Like how, how does that work out? Like, again, if you had no premarital agreement, what would happen to that

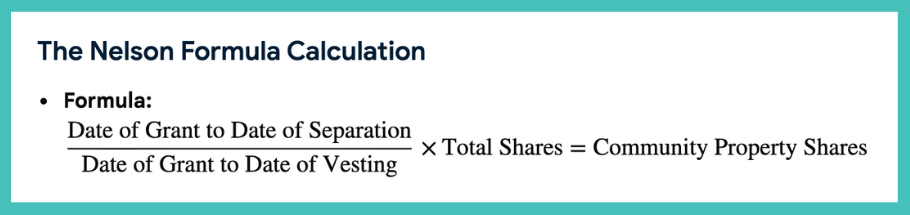

Katie: Yeah, this is another area that's like retirement accounts. Very, very simple and even very simple to calculate. So there's a formula, it's called the Nelson Formula, and it's a fraction and it's I think it's. Day, days between date of grant and exercise, I think is the numerator. I've got it written down on a sheet.

And then there's a denominator. And basically the way the fraction works is it makes it so it's not arbitrary. So the date of vesting is in there. That's a, that's an important date in the fraction. So. It comes up with a product 'cause you're taking a fraction and multiplying by the number of shares and you do this per tranche.

So you just have the number of community shares coming outta that fraction. So if something vests early in the marriage actually I have to be careful how I say this 'cause I always just sit down and do it. It's hard to describe it conceptually, but it's a very simple fraction. You just have. You know, a subtraction on the numerator, a subtraction or addition on the dominator.

Multiply it by the number of RSUs in the tranche, and then that's what the community shares are. And once you know what the community shares are, the shareholder can either decide they wanna buy the other party out of the shares or, which is usually what happens, but sometimes the other party wants to keep the shares and then you have to negotiate how.

Because the shareholder often will have, or, or is the one who has control over when they sell and all that kind of thing. So you have to have a process in place for how that's gonna be as fair as it can possibly be. But, but in a divorce context, that is the law and there is no other law unless. They agree to something else.

So if you're in a premarital agreement context or a postmarital agreement context people don't usually change the formula. It's either that they just wanna keep. Anything that vests as their own, but that doesn't really come up as much as you might think because the RSUs sort of functionally operate like income.

Right. So it's, it's not, they're not getting the asset in the same way. I mean, they are getting their shares, but I think because it's very simple to figure out in divorce and they're not, you know, no one's taking the whole thing. It's, it actually is one of the easier things.

Jenni: so it sounds like there's a set formula for this and, and if I'm understanding this correctly, conceptually, is it really about when this stuff vests? So if it vests during marriage, then it's considered part of the pro community property, and if it's vest before marriage, then is it not considered part of it?

Am I understanding that correctly?

Katie: Yes. So actually I'm gonna tell you the formula. I just pulled it up. So it's the numerator is days between the date of grant and the date of separation. The party separation and then the denominator is days between the date of grant and date of exercise. And then you multiply that by the number of shares, exercisable, and that's how you have the community property shares.

So so yes, so it's, it's if something vests and then you are getting separated the next day it, the other party's not gonna have

Jenni: I see. So it's also based on like how long this thing has been sitting around in your marriage as a, as a, as a asset, right? Like that's what

Katie: Yes. Exactly.

Jenni: that's what this, that's what this ratio is calculating.

Katie: Exactly, exactly. So you just do the formula and it never fails you. Which is why it's always hard for me to remember what it is, but or you, conceptually how it works. 'cause I just do it. But yeah, you just do it for every tranche and then that's, you know, and if it's, if it's super, I mean, it's never complicated, but sometimes it's.

So many tranches that you just have a forensic accountant do it. But it is that simple. That is the

Jenni: Gotcha. And I suppose this applies for both private and public shares, right? It's still a matter of like, if this is your founder shares that you received right away, then it kind of fell the same formula. How long was it in your

Katie: If it's something that vests, yes. Mm-hmm.

Jenni: , Okay, let's talk about kind of just family planning, long-term expectations.

How can you help, how does a pre premarital agreement help when you are bringing together safe, blended families, children, things from other relationships?

Katie: This is one of the best ways to ensure funds saved with one family. Don't deplete when a second family begins or joins the first family. It is one of the, you know, if there was, if somebody was widowed or divorced and they have started a family and funds for college and you know, whatever else.

I've had this situation where kids were almost on their way to college. There was a divorce and then there's a new marriage and. The party with the kids ready to go to college was pregnant with the new, soon to be spouse. So you have to think about those college funds, but also now you're preparing for a baby and bringing that baby into your life and you know, all the expense that that entails.

So it is actually one of the best uses of a premarital agreement because you don. You set yourself up to not have those sticky fights or, you know, that sort of like short fitted sheet of if there's not enough money to go around, what have you decided, you know, for each, for each, how you're gonna allocate each of those.

So it's a really, really good use for that scenario.

Jenni: Got it. Yeah, I can imagine. Are there ways to use premarital agreements to clarify expectations around things like childcare, career sacrifices, who steps back from work when kids arrive?

Katie: A career sacrifice is yes you can place a cap on earning capacity for spousal support, imputation purposes. So if if you have a divorce and you have no premarital agreement, then. If a party's asking for child and or spousal support, both parties to that spousal support dispute or agreement would have to be earning at their capacity.

And if anybody's under earning, then the court would eventually impute income to them as though they were earning at their capacity. So sometimes what I'll do in a premarital agreement is if somebody knows they're gonna be stepping out of the paid workforce to raise children full-time. We will cap their earning capacity for those years that they do that.

And of course they don't know what years those will be. You can't forecast that. But that there will be a cap on that so that they are actually, they can confidently step back and not worry about that piece of, you know of the equation. So that's one thing people can do.

Jenni: I could be being a little bit slow, but I didn't fully understand that. Like, can you give it to me like in a, like an example, like a specific example of a.

Katie: so if somebody knows, if somebody has a salary where they're fully earning right now, and they know that they're going to step back to take care of children full-time, lose their salary, if they were to separate. During that time, then the court would eventually say, not the first day, but they would say, we're going to impute income to you at some point.

'cause you're asking for spousal support and or child support. And

Jenni: Okay.

Katie: so you can, in the premarital agreement, put a cap on or even say there will be no imputation of income. So you treat it as though. The person really has no income and you don't even, 'cause, I mean, a lot of times the courts right outta the gate will at least impute minimum wage because whether they're expecting you to actually go out and get a minimum wage job, they know you could.

So you can, you can cap it, you can minimize it, but that's a way to make sure that you're not disadvantaged by financially in that sense, by stepping back

Jenni: I see. I see. Okay. So just to kind of put this as an example would be like, let's say one spouse. Plans to step back work. They used to be making $500,000. If you did nothing, then if there was a divorce, the court would say, well, you could go earn five, $500,000. And so would therefore reduce or maybe eliminate any spousal support.

But you could set an agreement where it says, look, I'm actively stepping back. So acute, no, or very, or more, less income because I'm stepping back and that's the truth that I cannot or am not earning that income, so therefore I should get more spousal support. Is that, is that the

Katie: Yes, and you have to, you have to draft it with specificity because of course that can't be forever. So if the separation happened and, you know, the kids were of an age where that care wasn't required, you know, I mean, you have to, you have to really think carefully about how you're drafting it so that, because.

That's a place where a judge could come in and say, this is unconscionable. You know, you're, you're setting this person up to pay you support for the rest of your life because you took two years off or something like that. So you have to think about those things, but that's an example of something I've done in terms of, you know, expectations around childcare.

Nothing like, I mean, you wouldn't put in a premarital agreement. Here's who's going to. Stay home with the kids or something like that because the judge can't enforce that. They can't force you to do that. So nothing like that. Yeah. Not the childcare piece, but just the piece around that loss of income and how you're gonna address that. And we haven't talked about in this interview, spousal support waivers or spousal support limitations. But those are available in premarital agreements. They're, they're risky because. They're so forecasting that they're kind of, it's an easy one for judges to say, I, this is, it feels unconscionable because there's no way, when this person made the agreement, they couldn't have known what the circumstances would be when they said, I don't need spousal support.

You know? But those are, those do exist, and you can do them with, you know, huge disclaimers. You know, there's, of the 30 pages, those get a whole page to really just disclaim it, but. Yeah, you can do things like that.

Jenni: Got it. Okay. All right. So what if a couple's already married and they're like, oh, we never did a premarital agreement. When might a postmarital agreement make sense? Mm-hmm.

Katie: It might make sense. A lot of times they happen because there's been some strain in the marriage and one of the parties says, or maybe both says, I will stay married to you, but I'm gonna. Not be as naive as I was the first time, and now I'm gonna put some, you know, some ideas in place. So because the parties are fiduciaries to each other once they're married, postmarital agreements have higher scrutiny on them than premarital agreements.

Do they also have higher scrutiny on them? Because there's inherently the idea that maybe there's more duress because the people are already married. It's more really the first thing that they're fiduciaries, but. There's sort of an idea that before they're married there's not really that much dress because they can always call off a wedding, you know, stressful as that might be.

So, 'cause you're always having to prove. The, the default presumption is that one or both parties signed this thing under duress because it's so prescriptive for their divorce. So yeah, so there's, so post marital agreements are weaker. They're still incredibly valuable, but, but the place where I don't advise them is if somebody's just.

Stressed about all the wedding planning, and they're like, how about if we just do this as a postmarital agreement? I'm like, no, that's a terrible reason to do a postal agreement. Every other reason makes complete sense to me. They are way more valuable than having nothing. But if, if it's just a matter of getting across the finish line before the wedding?

No, we do a premarital agreement.

Jenni: Okay, that makes sense. Okay. So, you know, if a couple is listening to this and they're like, Hmm, maybe this is something I wanna do, but I'm not totally sure if I need to do this. This is really necessary. Like, what are some of the questions they should ask themselves and what are the steps that they should take next? Mm-hmm.

Katie: They should. You know what I do in my office is I do a 10 minute free intake and usually, I mean, the overwhelming majority of the time after the intake, they either decide they're gonna hire me or not. I always offer too, I can charge you for a consultation where we really talk about some of these things and we talk through whether you should do it or not.

Because the intake, I'm not giving advice. I'm just telling them kind of how the process works. And so I have had people take me up on that because either they're not sure they wanna do it or not, or they just really wanna talk through the steps. And some of the times that's the people who wanna be really generous and they wanna just really talk it through.

Even though I say to them, you're gonna get the advice once you've paid, but you could, you could, you're welcome to pay me for an hour of my time. So that's one thing people can do. The other thing is. If they know in lay terms what they wanna do. Of course some of those things might change once they talk to a lawyer, but I always say, if you two are aligned at least in the spirit of what you wanna do, then if the terms change a little bit, because it doesn't really make sense legally what you're talking about, you still will have gotten on board with each other.

And that's one of the most important things because. Most of the people who draft premarital agreements, the lawyers are reasonable people not looking to fight. And I actually recommend attorneys for the other side and I, they're people I've known for decades and done a bunch of these agreements with, and those people definitely don't cause trouble and fight.

But regardless of who it is, it's always better if the couple is aligned because especially when it's something that's a little like, I'll say, you know, you two should really talk because that is gonna concern the other lawyer. And you're telling me it's ironclad. You both feel good about it, you know, so that's something where if it's gonna concern the other lawyer.

By the time she goes to her client, if you two are aligned, then it's not, I mean, she's not gonna cause a problem over it if her client is fine with it. And if it's not so egregiously bad, which it wouldn't be, or I wouldn't be letting it happen then you know, so that's the biggest thing I say is talk to each other.

And even if you don't know what the law is, you, you have a general sense of what it is you're trying to protect.

Jenni: Okay, so help me understand the process a little bit. Is it just one party who's working with you and the other party has to go find their own lawyer? Do you sit with the couple together? How does it work?

Katie: I only do two, two parties with attorneys. So I only do, I only represent one side of it. There are lawyers who will do mediated agreements. I don't love the idea of those for a few reasons. One is that you still end up with, you actually end up with three lawyers instead of two because nobody will do a mediated agreement where the two parties don't each have their own separate lawyer.

So you end up with more lawyers than fewer. And the other reason is that with the consulting attorneys, if someone does mediation with consulting, now this is my bias. I've, I've talked to my colleagues who don't feel this way at all, but. When I've offered to do consulting for a mediated agreement, the potential client every single time has said, we're already completely happy with the agreement.

We just want you to sign it. And I say, that's, I worked too hard for my law license. I'm not doing that. You know, I'm not, you know, they're really looking to not pay more money 'cause they already paid a lawyer. So my belief is that judges know. Or assume that if you just did a mediated agreement and your lawyer just kind of rubber stamped it that that's the way they look at it.

'cause that's the way I look at it. So I always feel better knowing. So I've actually never mediated one or accepted a consulting engagement because or I have accepted consulting engagements, but. Under different circumstances, but I have really landed on the place where I say, no, I, the right thing for me is to have one attorney on each side.

You're double checking each other.

Jenni: Yeah. Got it. Okay. That's helpful. So basically, so one, basically one spouse or one partner would hire you and then you, if you need, they need to find somebody else. You have some references that you could give to for the other party. And then just generally speaking, I know, I'm sure it depends, but like roughly speaking, what is the cost?

How long does this take to actually get this thing done?

Katie: Well, with me, it doesn't depend, although it can change, but I do a flat fee because I just, I, I just do. So I do a flat fee of 8,500 and that's where, when I was saying earlier that, you know, some people will say, oh, but we have a really simple situation. It doesn't matter. I'm doing the same work. So and the only time that changes and it has changed is if.

Something. So it's rare, but something so unexpected happens that it's like, okay, this is gonna be astronomically more work, and then I will amend it where they're doing a second flat fee or. The timing, it goes on so long for reasons outside of my control. Basically I lose track of my client. They don't get back to me.

And then it's like, okay, we need to, if we're resuming this, we need to, you know, you need to pay me a little more. But but I just, the reason I do a flat fee is because I, I felt like people always, always wanna know what's it gonna cost? And that's a question I really can't answer with any. Veracity because there's another side involved.

So I can't, I, I have no idea. And people just didn't like hearing that. And then they wanted a range and I said, I'm not. No, I'm not doing that. I'm not. I'm, I'm not. So then I just decided on a flat fee. And you know what, sometimes I eat it and sometimes I don't, but it's like, I feel good about that and it, it makes people more comfortable.

They just pay that upfront. But most lawyers do a retainer against hourly. And I know some lawyers are more comfortable than I am with giving a range or even an expectation of what it will cost. I just, I've already done my stats and I know there's no way to accurately

Jenni: Got it. Okay. But like in, I guess just to ballpark it, it's kinda like 8,500 for you and then potentially they hire someone else. Could be similar range of something, whatever

Katie: No, no, that's what I'm saying. I, I, I say there's no

Jenni: Okay. All right. So it's whatever the other lawyer is, is, is deciding to quote or it

Katie: It's however many hours it ends up being. So I just set my flat fee. It's, it's, it's not a statement of what it costs at all. It's just really, I just decided I was gonna do a flat fee and. That's, that's what I did. But no, it's, it's gotten substantially higher than that before. Not usually lower, but but yeah, there's not, I've never felt comfortable giving a range because I've looked at, I've looked at my past ones and it's not even, like I was saying before, it's not even complexity of assets or income at all.

Jenni: it's maybe how long the couple needs to get to a place that they're happy with.

Katie: yeah. And parents being involved. And like I said, I don't talk to the parents, but there's a lot that happens there too. Yeah. There's really no predicting based on what they have.

Jenni: Great. Okay. And then I guess like just a couple of two more closing questions. Just like thinking about, you know, if someone's listening to this and they're like, oh, well that is a fair amount of money, and I, and I know this is will be difficult question for you to answer, but like, is there a level of assets, I, I mean maybe you can just based on your own clients, right?

Like the typical level of assets that we're talking about that would engage in something like this? Or is that a bad question?

Katie: not a typical because it doesn't. I mean for sure people when they have, when they know they're gonna inherit substantial wealth or they already have substantial wealth, they do it. But no, because people are really protecting things for different reasons and an amount of money that doesn't sound like a lot to some people, is a lot to someone else.

And you know, a lot of times I have parents paying my fee also. People's fiance can pay my fee. There's nothing ethically against that. So it doesn't, I mean, someone can still want protection or still wanna go through this process 'cause their fiance wants to protect what they have and it doesn't, it doesn't necessarily translate except, like I said, the obvious that if, if the higher the level of wealth.

I don't really ever, well, I have had somebody not do it. They just didn't wanna part with that money. But my, my very strong belief, just because I also handle divorces, is if you can afford it at all, you should do it. And it doesn't really matter because that money is gonna matter to you. So it doesn't matter how much that money is.

Jenni: yeah, that makes sense. I mean, the thing is you all think nothing bad will happen, but if it does, this is a small amount of money to pay for, you

Katie: Right.

Jenni: the, the terror that can

Katie: thing, unless the only thing you have in life and will ever have is $8,500,

Jenni: Yeah.

Katie: then it just doesn't make sense to say that's what you know because you're Yeah. Yeah, exactly. You will make it back in what you don't pay out. And you know, as I said before, if the thing is well drafted, you're just skipping right over the whole divorce.

I mean, you still have to do the divorce process, but you're not, you're

Jenni: And I be fighting, and I mean, I've been through by, by through friends or through clients and seen that process and it's. And it's cost. Like one of the most, you could say one of the biggest wealth destroyers is a divorce, right?

Katie: Yes. Yes. And what I should say too is you can't make provisions around child custody, visitation, things like that in a premarital agreement or postmarital agreement. There's just no forecasting there. There's no way to do it. And it's also. Children are humans and you know all that. But so because of that, you may still have a contentious, ugly divorce, but the assets and income and all that kind of part of it will be well settled.

Jenni: right. Got it. Okay. Well this is great. Are there any, is there anything else that I haven't asked that you think our listeners should be aware of?

Katie: No, I think you did a good job of covering the ground.

Jenni: Okay. So what is the best way for people to reach you if they want to learn more?

Katie: They can email me at katy@burkelawsf.com. That's K-A-T-I-E at B-U-R-K-E-L-A-W sf.com. Or they can call my office at (415) 997-6665.

Jenni: Okay. Awesome.

Katie: Thanks,

Jenni: great. Okay. Thank you. That was fun.

Another misconception is that attorneys just pull a generic form. I use templates I’ve built over time, but every agreement is customized.

Another misconception is that attorneys just pull a generic form. I use templates I’ve built over time, but every agreement is customized. Q: Anything specific for LGBTQ+ couples?

Q: Anything specific for LGBTQ+ couples? Jenni: Where do you see people get caught off guard?

Jenni: Where do you see people get caught off guard? Jenni: What are a few examples of things that become harder without an agreement?

Jenni: What are a few examples of things that become harder without an agreement?

Jenni: If a couple isn’t sure they need an agreement, what should they do next?

Jenni: If a couple isn’t sure they need an agreement, what should they do next?